Take a minute and take a hard look at your portfolio and ask yourself…

“Are you investing like the middle class, or are you investing like the wealthy?” It’s well documented by groups like Tiger 21 that the ultra-wealthy investment allocations are very different from those of the middle class.

I know you’ve heard this ad-nauseum, but the rich are rich because they do things differently than the middle class, and contrary to popular belief, most millionaires are self-made and didn’t just fall into wealth.

From early on, the rich decided to break away from the pack, and to do so; they would have to go against the middle-class grain and buck the habits, attitudes, and biases that burden the middle class.

The middle class’s common investing habit that the rich avoid is devotion to a 60/40 portfolio (60% stocks/40% bonds). The fact that the 60/40 portfolio is still going strong speaks to how ingrained it is in the middle-class psyche. There’s no reasonable justification for a 60/40 portfolio in the current economy, yet it is still going strong. The 60/40 portfolio is a hedging strategy.

The idea is that since stocks and bonds generally move in opposite directions, when one asset is down, the other will compensate in the opposite direction. This allocation may have worked in the ’80s when treasury rates hovered near 10%, but that rule no longer makes sense today where the 10-year treasury currently hovers around 1.7%.

Over the past 20 years, a 60/40 portfolio delivered on average an annual return of 5.4%. The average yearly inflation during that period was 2.5%. That’s an average annual net return of 2.9%. You can’t get rich at those rates, and that’s why the rich avoid the 60/40 portfolio.

So, if you can’t get rich from the 60/40 portfolio, why is it so popular?

Human behavior and biases have a lot to do with it. There’s a cognitive bias in behavioral science that explains why the middle-class cling to the 60/40 portfolio. It’s called inconsistency-avoidance tendency. In plain English, it means humans hate change.

Humans are reluctant to change, and as a result, it’s hard for many of us to eliminate bad habits. The so-called Anti-Change Bias may have served the primitive man who found safety in groups from predators. Breaking from the crowd made our ancestors vulnerable, so nobody did it.

Anti-Change is one bias that would explain middle-class investing habits. Another bias is the Availability Bias. The Availability Bias says we do what’s easy and listen to whatever advice we hear the loudest and most often. That means whatever dominates cable news, the financial press, and social media will garner the middle class’s attention.

The 60/40 portfolio is what Wall Street and its minions push, and the middle class doesn’t bother fighting it because they don’t like change, and it takes too much energy to break from the crowd.

Like the Anti-Change Bias, the Availability Bias is an energy-conserving strategy that’s part of the self-preservation instinct. Not having to think too hard conserves energy to flee from predators is the thinking.

Like the 60/40 portfolio is obsolete as a useful allocation strategy, the Inconsistency Avoidance Tendency and the Availability Bias are both obsolete self-preservation strategies. Going with the crowd has never been more dangerous. Those who dare to break away are the ones who will survive financially.

Warren Buffett has made a career of going against the grain. He has long advocated investors to zig when others zag by encouraging investors to: “Be greedy when others are fearful.”

The rich aren’t afraid to break away from the crowd, and that is the very first step to take to invest like the rich – to zig when the middle-class zags. While the middle-class chases stocks and bonds, the rich reach for alternatives – literally and figuratively.

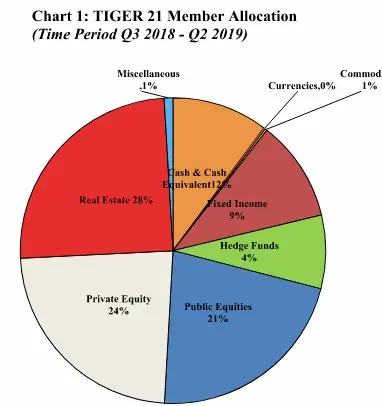

For insight, the following chart illustrates the typical asset allocation of the ultra-wealthy.

While the middle class allocates 60% or more to stocks, the ultra-wealthy allocate less than a quarter to equities, with the overwhelming majority allocated to the big two alternative asset classes:

- Real Estate (28%).

- Private Equity (24%).

To be rich, invest like the rich.

The first step to investing like the rich is recognizing that the way the middle class has been investing doesn’t work.

The 60/40 portfolio only makes financial advisors rich. Those with the courage to break free of middle-class investing biases and tendencies will find the financial independence and wealth prize they’re seeking.